Gold what matters

Silver Manipulation

Documented legal rulings:

JPM 920 Mio 2023

DB 38 Mio 2016 spoofing

4 Tactics

Paper market Manipulation

Annual Production 850 Million Ounces

Short Positions 60 Billion Ozs

Prize Slams

during NY Mornings

Spoofing and Collusion

Coordination 11 AM Rule

Options Expiry Manipulations

worthless expiries

Net short positions

211 Mio ozs vs Global mine 900 Mio ozs

Physical supply deficit 700 Mio ozs

LBMA no inventory

Physical Demand

Physical and manufacturing demand

Delivery shortages

source physical silver beyond market

Inventory depleted (LBMA, Comex, Shanghai)

physical demand is exceeding available inventory

Gold Silver Ratio

Ratio is below 75 means Silver is demanded more than Gold Stress is increasing

Premiums are rising Physical drawdowns

Solutions for the shorts.

Cover the shorts

Offer Cash Settlements

source physical silver

margin hikes

Investment demand increasing

Coins and Bars

Industrial demand

Military Needs

Solar panels

Electronics

EV battery needs

China stopped silver outflow

Summary outlook

watch Comex Inventory 40 - 60 mio

watch Premiums

watch Gold Silver Ration below 75 is momentum shift

watch test of market level above 50 is bullish

watch CFTC data if short positions are falling is bullish

UNGEORDNETER RESET MIT GOLDAUFWERTUNG UM EIN VIELFACHES

Von Egon von Greyerz

Tektonische Verschiebungen liegen vor uns. Sie werden eine Schuldenkrise in den USA und Europa umfassen und in einem Schuldenkollaps sowie einem steilen Fall des Dollars und Euros enden, wobei Gold einen Platz als Reserveanlage einnimmt – allerdings zum einem Vielfachen des heutigen Preises.

Die nächste Phase des westlichen Niedergangs ist angebrochen und wird sich bald verschärfen. Die absurden Sanktionen gegen Russland haben diesen Verfall beschleunigt und angeheizt. Die Sanktionen machen Europa schwer zu schaffen, zeigen aber auch in den USA Wirkungen, die dort nicht erwartet wurden, aber für einige von uns klar absehbar waren. Die Römer hatten verstanden, dass Freihandel zwischen den von ihnen eroberten Ländern essentiell war. Die US-Administration hat jedoch das Geld und die Fähigkeit, Länder, die man nicht mag, im Handel zu blockieren.

Doch wer sich selbst ins Knie schießt, bekommt wirklich Schmerzen; und die Konsequenzen sehen wir direkt vor unseren Augen. Im Rest der Welt wird niemand mehr US-Schulden oder Dollars halten wollen. Das ist ein katastrophales Problem für die USA, weil deren Defizite in den kommenden Jahren exponentiell wachsen werden.

Also: Ein Schuldenkollaps ist nicht nur eine drohende Katastrophe, sondern eine Bombe, die mit Überschallgeschwindigkeit auf die US-Wirtschaft zuschießt.

Angesichts des drohenden Untergangs des Petrodollars und der Explosion der US-Verschuldung gibt es nur eine Lösung für den staatlichen Finanzbedarf der USA: Die Federal Reserve wird als alleinige Käuferin von US-Staatsanleihen einstehen.

EINE KATASTROPHALE TODESSPIRALE

Also: Die SCHULDEN-Spirale – höhere Schulden, höhere Defizite, mehr US-Staatsanleihen, höhere Zinssätze und fallende Anleihepreise – wird sich bald in eine Todesspirale verwandeln: einbrechender Dollar, hohe Inflation und höchstwahrscheinlich Hyperinflation. Für mich klingt das nach Schuldenausfall, obwohl dieses Wort wohl niemals offiziell benutzt werden wird. Es ist schwer Niederlagen einzugestehen, selbst wenn man sie selbst schon sieht!

Ja, die USA werden die Situation möglicherweise mit CBDC (Zentralbankdigitalwährungen) verschleiern. Da diese aber auch nur eine weitere Form von Fiat-Geld sind, werden sie bestenfalls etwas Zeit schinden, das Endergebnis wird letztlich aber dasselbe sein.

US-SCHULDENOBERGRENZE-FARCE GEHÖRT AUF DEN BROADWAY UND NICHT AN DIE WALL STREET

Die Schuldenobergrenze (debt ceiling) wurde 1917 geschaffen, um rücksichtslose Staatsausgaben in den USA einzuschränken. Trotzdem geht diese Farce seit 106 Jahren weiter. Während dieser Zeit herrschte in den amerikanischen Regierungen und im US-Kongress totale Geringschätzung für Haushaltsdisziplin.

Das Problem sind nicht nur die Schulden an sich, sondern auch die Kosten der Schuldenfinanzierung.

Auf das Jahr gerechnet betragen die Finanzierungskosten der US-Bundesschuld aktuell 1,1 Billionen $. Wenn wir, vorsichtig geschätzt, in den nächsten zwei Jahren von einem Anstieg der Verschuldung auf 40 Bill. $ bei einem Zinssatz von 5 % ausgehen, dann wären das 2 Billionen $. Das wären 43 % der Steuereinnahmen. Und das zu einem Zins von 5 %. Welcher wahrscheinlich zu niedrig ist, da die Inflation steigen wird und die US-Notenbank die Kontrolle über die Zinssätze verliert.

Somit kommt ein sehr düsteres Szenario auf uns zu; und das ist mit Sicherheit noch kein Worst-Case-Szenario.

DIE FED: WAHL ZWISCHEN PEST UND CHOLERA

Die Federal Reserve und die US-Regierung stecken jetzt zwischen Skylla und Charybdis (Pest oder Cholera).

So wie es heute aussieht, werden die USA in den nächsten Jahren abwechselnd gegen Skylla und dann gegen Charybdis prallen, solange, bis das US-Finanzsystem aber auch die US-Wirtschaft immer härte Schläge einstecken und untergehen wird, so wie auch alle anderen historischen Geldsysteme.

Natürlich wird auch der Rest des Westens, wie auch das extrem schwache Europa, den USA in die Tiefe folgen.

BRICS UND SCO – AUFSTREBENDE MÄCHTE

Die gesamte Welt wird leiden. Doch rohstoffreiche Länder und die weniger verschuldeten werden den kommenden Sturm besser überstehen.

Dazu zählen große Teile Südamerikas, der Nahe Osten, Russland und Asien. Die expandierenden Machtblöcke der BRICS und der SCO (Shanghai Cooperation Organisation) werden die starken Mächte sein, wo ein zunehmend großer Teil des globalen Handels stattfinden wird.

Abgesehen von großen politischen und geopolitischen Umbrüchen wird China zur dominanten Nation und zur wichtigsten Fabrik der Welt. Auch Russland wird wahrscheinlich zu einer großen Wirtschaftsmacht werden. Mit 85 Billionen $ in Rohstoffressourcen hat das Land eindeutig das Potential dafür. Doch zuerst muss das politische System Russlands „modernisiert“ oder restrukturiert werden.

Was ich hier beschreibe, sind natürlich strukturelle Verschiebungen, die Zeit brauchen, möglicherweise Jahrzehnte. Aber ob man will oder nicht, die erste Phase – der Fall des Westens – könnte schneller gehen, als uns lieb ist.

EIN GELDSYSTEM ENDET IMMER MIT EINER SCHULDENEXPLOSION

Im Jahr 1913 war die US-Gesamtverschuldung unerheblich, 1950 war sie dann auf 406 Mrd. $ angewachsen. Als Nixon 1971 das Goldfenster schloss hatten die USA 1,7 Billionen $ Schulden. Anschließend wurde die Kurve ständig steiler, wie man in Diagramm sieht. Ab September 2019 begann das US-Bankensystem auseinanderzubrechen, aus der Repo-Krise wurde dann die Covid-Krise, welche dem Staat einen viel besseren Vorwand bot, zusammen mit den Banken unbegrenzte Geldmengen zu drucken.

Somit stieg die US-Gesamtverschuldung allein in diesem Jahrhundert von 27 Bill. $ auf 94 Bill. $!

Aber das ist Geschichte, und wir wissen, dass sich an der Geschichte nichts mehr ändern lässt. Doch jetzt beginnt der Spaß erst richtig.

Seit einiger Zeit warne ich vor einer kommenden Schuldenexplosion. Und ich glaube, das war es jetzt.

In einem vor kurzem veröffentlichten Artikel über den Goldpreis habe ich erklärt, dass die finalen Phasen einer Hyperinflation exponentiell verlaufen.

„WIE LANGE BRAUCHT ES, BIS DIESES STADION VOLL WASSER IST?

ERST EIN TROPFEN PRO MINUTE / MIT JEDER MINUTE VERDOPPELT SICH DIE ANZAHL DER TROPFEN

BRAUCHT ES EINEN TAG, EINEN MONAT ODER EIN JAHR?

NEIN! ES BRAUCHT NUR 50 MIN.

WIE VOLL IST ES NACH 45 MIN? 75 -90 %?

NEIN, NUR ZU 7 % GEFÜLLT! ERST IN DEN LETZTEN 5 MIN. GEHT ES VON 7 % AUF 100 %!“

BRAUCHT ES EINEN TAG, EINEN MONAT ODER EIN JAHR?

NEIN! ES BRAUCHT NUR 50 MIN.

WIE VOLL IST ES NACH 45 MIN? 75 -90 %?

NEIN, NUR ZU 7 % GEFÜLLT! ERST IN DEN LETZTEN 5 MIN. GEHT ES VON 7 % AUF 100 %!“

Mit der kommenden Schuldenexplosion werden wir ein sehr ähnliches exponentielles Muster sehen. Wenn wir davon ausgehen, dass die finalen 5 Minuten der exponentiellen Phase im September 2019 begannen, dann war das Stadion damals nur zu 7 % voll und wird sich in den kommenden Jahren von 7 % auf 100 % füllen, bzw. die Menge wird, von diesen Ständen aus, um das 14-fache ansteigen.

Dabei handelt sich natürlich nur eine Demonstration und nicht um exakte Wissenschaft, dennoch zeigt sie, dass die US-Verschuldung theoretisch jetzt explodieren könnte.

Werfen wir also einen kurzen Blick auf die Faktoren, die diese Schuldenexplosion auslösen werden.

BANKENPLEITEN

Wie das Hoover Institute in einem Bericht errechnete, sind bei aktuell mehr als 2.315 US-Banken die Aktiva weniger wert als die Passiva. Der Marktwert ihrer Kreditportfolios liegt insgesamt mit 2 Billionen $ unter dem Buchwert. Und das, nicht zu vergessen, noch vor dem EIGENTLICHEN Fall der Aktivwerte, der noch aussteht.

Nehmen wir allein die US-Immobilienwerte, die von den Kreditgebern stark überbewertet werden:

Also: Die vier US-Banken, die kürzlich untergingen, sind wirklich erst der Anfang. Zudem darf niemand glauben, dass es hier nur um Kleinbanken geht. Auch Großbanken werden genau diesen Weg gehen.

Während der Subprime-Krise 2006-09 waren Bailouts die Norm. Doch damals hieß es, dass es in der nächsten Krise auch Bail-Ins geben werde.

Doch bislang haben wir in den USA noch keine Bail-Ins gesehen. Der Staat und die Fed waren eindeutig besorgt wegen systemischer Risiken und hatten nicht den Mumm, die Bankkunden an den Verlusten zu beteiligen, nicht einmal oberhalb der FDIC-Einlagensicherungslimits.

Ich bezweifele, dass die Bankeneinleger bei einer Ausweitung der Krise wieder so glimpflich davonkommen werden. Weder die FDIC noch der Staat können es sich leisten, alle zu retten. Stattdessen wird man den Einlegern einen Deal unterbreiten, den diese nicht ablehnen können – Guthabensausgleich durch den verpflichtenden Bezug von US-Staatsanleihen.

Der europäische Bankensektor befindet sich in einem schlimmeren Zustand als der US-Bankensektor. Europäische Banken sitzen auf großen Verlusten aus Anleiheportfolios, die zur Zeit der negativen Zinssätze erworben wurden. Zum aktuellen Zeitpunkt kennt niemand das wahre Ausmaß der Verluste, doch wahrscheinlich werden sie erheblich sein.

Auch in den Bereichen Geschäfts- und Wohnimmobilien ist die Situation in Europa schlimmer als in den USA, weil die europäischen Banken die meisten dieser Kredite direkt selbst finanzieren, darunter auch Wohnimmobilienhypotheken im Umfang von 4 Billionen €.

Zudem leiden diese Banken auch noch unter der Diskrepanz zwischen der niedrigen Hypothekenverzinsung und den gestiegenen Zinsen zur Eigenfinanzierung.

Jacques de Larosière, ehemaliger Chef der Banque de France und Ex-Vorstand des IWF, beschuldigt unterdessen die führenden Stellen, sie würden das private Bankensystem mit wahnsinnigen Mengen QE zerrütten, nachdem dieses toxisch geworden sei:

„Weit entfernt davon, für Stabilität zu sorgen, veranstalten die Zentralbanken eine Meisterklasse zum Thema, wie man eine Finanzkrise organisiert.“

3 BILLIARDEN $ GLOBALE VERSCHULDUNG & VERBINDLICHKEITEN

Wenn man die ungedeckten Verbindlichkeiten und das Gesamtvolumen laufender Derivate zur globalen Verschuldungssumme addiert, kommen wir auf ungefähr 3 Billiarden $, wie ich in folgendem Artikel deutlich mache:

„Das war’s! Das Finanzsystem ist unwiederbringlich kaputt“

Leider ist das westliche Finanzsystem heute zu groß, um gerettet zu werden aber auch zu groß, um zu scheitern.

Doch alle Mannen des Königs mit all ihren Pferden können es trotzdem nicht retten. Also: Auch wenn das System zu groß ist, um zu scheitern, so wird genau das passieren – mit sehr, sehr schlimmen Konsequenzen.

GOLD ERFÄHRT BEACHTLICHE AUFWERTUNG IM UNGEORDNETEN REST

Etwas mehr als ein Jahrhundert nach der Gründung der US-Notenbank und dem Beginn der Schuldenobergrenze hat der mächtige Dollar 99 % seines Wertes, gemessen an seiner Kaufkraft, verloren.

Gemessen am einzigen Geld, das im Laufe der Geschichte überlebt hat – Gold –, hat der Dollar ebenso 99 % verloren.

Das ist natürlich kein Zufall. Gold ist nicht nur das einzige Geld, das historisch überlebt hat, sondern auch das einzige Geld, das seine Kaufkraft über die Jahrtausende hinweg erhalten hat.

So kostete eine römische Toga vor 2000 Jahren eine Unze Gold, was heutzutage der auch der Preis für einen hochwertigen Männeranzug ist.

Man würde meinen, dass ein 99 %iger Wertverlust bei der Weltreservewährung ein Desaster ist. Und das ist es auch, allerdings haben sich die USA und die westliche Welt über exponentielles Schuldenwachstum angepasst, um diese desaströse Währungsentwertung auszugleichen.

Noch interessanter ist aber, dass Gold in diesem Jahrhundert um das 8- bis 10-fache gegenüber den meisten Währungen gestiegen ist.

Damit hat es, gegenüber praktisch allen großen Anlageklassen, eine überlegene Performance gezeigt.

Und trotzdem ist niemand Goldeigentümer; Gold macht nur 0,5 % der globalen Finanzassets aus.

Jüngst markierte Gold Allzeithochs gegenüber allen Währungen, einschließlich des Dollars.

Doch auch trotz der extrem starken Performance von Gold – oder korrekter ausgedrückt, trotz der anhaltenden Entwertung aller Währungen – redet niemand über Gold.

Schauen Sie sich unten die Zahl der Presseberichte an, in denen es um Gold geht (weiße Balken); sie bestätigen, dass die jüngsten Kursgewinne beim Gold (blaue Linie) nur ein Gähnen auslösten.

Und das ist natürlich sehr bullish. Stellen Sie sich vor, alle Aktienmärkte würden neue Hochstände markieren. Die Medien wären voll damit.

Das sagt uns aber auch Folgendes: Dieser Goldbullenmarkt, oder Bärenmarkt der Währungen, hat noch einen sehr langen Weg vor sich.

Wie ich nicht selten schreibe: Im Verlauf der Geschichte hat noch kein Fiat-Geld überlebt.

Goldpreisanstiege sind im Verlauf der Zeit garantiert, weil Staaten und Zentralbanken ausnahmslos immer ihre Währungen zerstören, indem sie praktisch unbegrenzte Mengen Falschgeld schöpfen.

Da das schon Tausende Jahre der Fall ist, lehrt uns die Geschichte, dass dieser Trend zur konstanten Entwertung von Fiat-Geld unverwüstlich ist, was an der Gier und der Misswirtschaft von Regierungen liegt.

So wie sich jetzt die Schuldenkrise beschleunigt, so wird sich auch der Goldpreis beschleunigen.

Luke Groman bringt einen sehr interessanten Punkt in seiner Diskussion mit Grant Williams (grant-williams.com im Abonnement). Groman meint, dass der Dollar als Reservewährungswert wahrscheinlich durch Gold ersetzt werden wird, auch wenn der Dollar als Transaktionswährung noch nicht am Ende ist.

Diese Kombination aus Dedollarisierung und Liquidation von US-Staatanleihen durch ausländische Halter wird zu einer solchen Entwicklung führen.

Rohstoffländer werden beispielsweise Öl an China verkaufen, dafür Yuan erhalten und diese Yuan an der Shanghaier Goldbörse in Gold eintauschen. Dann halten sie Gold statt Dollar. Damit meiden sie den Dollar als Handelswährung im Rohstoffbereich.

Damit Gold als Reserveanlage funktionieren kann, wird es mit einer Null am Ende und einer größeren Zahl am Anfang, so sagt es Luke Groman, aufgewertet werden müssen. Die Idee wäre im Grunde, dass Gold zu einem neutralen Reserve-Asset wird, das in allen Währungen schwankt.

Das umgekehrte Dreieck (siehe oben), wo die globale Verschuldung sich nur auf 2 Billionen $ Zentralbankengold stützt, macht eine Gold-Aufwertung augenscheinlich.

Als Reserve-Asset ist ein flottierender Goldpreis natürlich viel vernünftiger als ein festgelegter Goldpreis, der die Währungen deckt. Dies käme dem Konzept von Free Gold am nächsten.

Lesen Sie dazu auch meinen Artikel von 2018: „Freigold wird Papiergold-Kasino vernichten“

Sollte Gold zu einer Reserveanlage werden, so hätte das auch zur Folge, dass es von den heutigen Ständen ausgehend um, sagen wir, das 25- oder 50-fache steigen würde. In heutigem Geld wäre das sicherlich kein unmögliches Ergebnis. Die Entwertung des Dollars und der westlichen Währungen werden wahrscheinlich einen ähnlichen Effekt haben, doch dann gehen wir schon nicht mehr vom heutigen Geld aus. Die Zukunft wird es zeigen.

Da Gold sich in einer Beschleunigungsphase befindet, werden wir wahrscheinlich deutlich höhere Kursstände sehen, ganz gleich wie lange das dauert und aus welchem Grund es steigt.

Der 1980er Goldpreis von 850 $ läge heute, bereinigt um die tatsächliche Inflation, bei 28.300 $.

Da Gold sich heute in einer Beschleunigungsphase befindet, werden wir viel höhere Stände sehen, ganz gleich wie lang es braucht.

Klar ist, dass Fiat-Geld, Anleihen, Immobilien und Aktien allesamt gegenüber Gold steil fallen werden.

Für Investoren ist es wichtig, sich abzusichern gegen den bedeutendsten RESET der Geschichte, der ein ungeordneter Reset sein wird.

Falls Sie also noch kein Gold haben, dann schützen Sie bitte Ihre Familie und ihr Vermögen, indem sie physisches Gold erwerben.

Die Neupositionierung von Gold als globaler Reservewert könnte schrittweise geschehen oder aber ganz plötzlich passieren. Doch seien Sie bitte vorbereitet, denn wenn es passiert, sollte man lieber kein wertloses Papiergeld und keine wertlosen Papier-Assets mehr halten.

THIS IS IT! – THE FINANCIAL SYSTEM IS TERMINALLY BROKEN

By Egon von Greyerz

The financial system is terminally broken, toast, kaput!

Anyone who doesn’t see what it happening will soon lose a major part of their assets either through bank failure, currency debasement or the collapse of all bubble assets like stocks, property and bonds by 75-100%. Many bonds will become worthless.

Wealth preservation in physical gold is now absolutely critical. Obviously it must be stored outside a broken financial system. More later in this article.

The solidity of the banking system is based on confidence. With the fractal banking system, highly leveraged banks only have a fraction of the money available if all depositors ask for their money back. So when confidence evaporates, so do the balance sheets of the banks and depositors realise that the whole system is just a black hole.

And this is exactly what is about to happen.

For anyone who believes that this is just a problem with a few smaller US banks and one big one (Credit Suisse), they must think again.

RE CREDIT SUISSE SEE ‘STOP PRESS’ AT THE END OF THE ARTICLE.

THE BANKS ARE FALLING LIKE DOMINOS, INCLUDING CREDIT SUISSE TONIGHT

Yes, Silicon Valley Bank (16th biggest US bank) is gone after an idiotic and irresponsible policy to invest short term customer deposits in long term US Treasuries at the bottom of the interest rate cycle. Even worse, they then valued the bonds at maturity rather than market, to avoid taking a loss. Clearly a management that didn’t have a clue about risk. SVB’s demise is the second biggest failure of a US bank.

Yes, Signature Bank (29th biggest) is gone due to a run on deposits.

And yes, First Republic Bank had to be supported by US lenders and the Fed by a $30 billion loan due to a run on deposits. But this won’t stop the rot as depositors attack the next bank and the next one and the next one……….

And yes, the Swiss second largest bank Credit Suisse (CS) is terminally ill after a number of poor investments over the years combined with poor management that has come and gone virtually every year.. I wrote an important article about the coming demise of CS 2 years ago here: “ARCHEGOS & CREDIT SUISSE – TIP OF THE ICEBERG.”

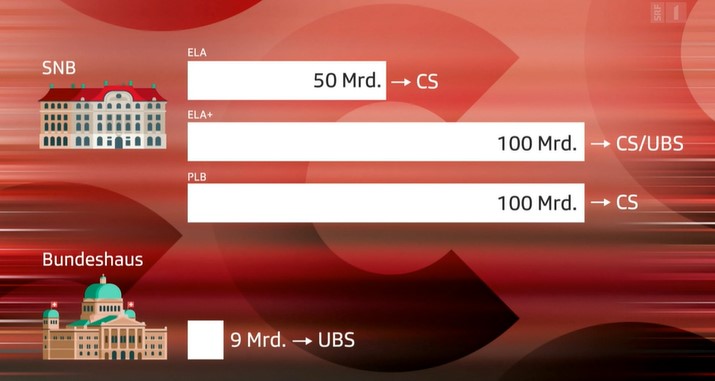

The situation at CS is so dire that a solution needs to be found before Monday’s (March 20) opening. The bank cannot survive in its present form. A failure for Credit Suisse would not just rock the Swiss financial system but have severe global repercussions. A merger with UBS is one solution. But UBS had to be bailed out in 2008 and doesn’t want to be weakened again by Credit Suisse without state guarantees and support from the Swiss National Bank (SNB). The SNB injected CHF50 billion into CS last week but the share price still went to a new low.

No one should believe that a state subsidised takeover of Credit Suisse by UBS will solve the problem. No, it will just be rearranging the deck chairs on the titanic and making the problem bigger rather than smaller. So rather than a lifebuoy, UBS will have a massive lead weight to carry which will guarantee its demise as the banking system collapses. And the Swiss government will take on assets which will be unrealisable.

Still, it is likely that by the end of the present weekend a deal will be announced with UBS being offered a deal they can’t refuse by taking over the good assets and the SNB/Government nurturing the bad assets of Credit Suisse in a rescue vehicle.

The SNB is of course in a mess itself, having lost $143 billion in 2022. The SNB balance sheet is bigger than Swiss GDP and consists of currency speculation and US tech stocks. This central bank is the world’s biggest hedge fund and the least successful.

Just to put a balanced view on Switzerland. It has the best political system in the world with direct democracy. It also has low Federal debt and normally no budget deficits. It is also the safest country in the world.

SWISS BANKING SYSTEM TOO BIG TO SAVE

But the Swiss banking system is very unsound, just like the rest of the world’s. A central bank which is bigger than the country’s GDP is extremely unsound. And a banking system which is 5x Swiss GDP makes it too big to save.

Although the Fed and ECB are much smaller in relation to their countries’ GDP than the SNB, these two central banks will soon discover that their assets of around $8 trillion each are grossly overvalued.

With a global banking system on the verge of a systemic failure, Central Bankers and bankers have been working around the clock this weekend to temporarily avoid the inevitable collapse of the bankrupt financial system.

BIGGEST MONEY PRINTING IN HISTORY COMING

As I pointed out above, the main Central Banks would also be bankrupt if they valued their assets honestly. But they have a wonderful source of money that they will tap to save the system.

Yes, I am of course talking about money printing.

We will in coming months and years see the most massive avalanche of money printing that has ever hit the world.

For anyone who believes that we are just seeing another bank run that will quickly evaporate, they will need to take a shower in ice cold Alpine water.

What we are witnessing is not just a temporary drama that will be sorted out by “the all powerful and resourceful” central banks.

THE DEATH OF MONEY

No, instead what we are seeing is the end phase of this financial era which started with the formation of the Fed in 1913 and in the next few years, or much sooner, will end with the death of money.

But the Death of Money doesn’t just mean that the dollar (and most currencies) will make their final move to ZERO, having already declined 98% since 1971.

Currency debasement is not the cause but the effect of the banking Cabal taking control of the money for their own benefit. As Mayer Amschel Rothschild said in the late 1700s: “Let me issue and control a nation’s money and I care not who makes the laws”.

Sadly, as this Cassandra (me) has written about since the beginning of the century, the Death of Money is not just all currencies going to ZERO as they have throughout history.

No, the Death of Money means a total and final collapse of this financial system.

Cassandra was a priestess in Greek mythology who was given the gift of predicting major events accurately but also given the curse that no one would believe her predictions.

No depositor must believe that the FDIC (Federal Deposit Insurance Corp) in the US or similar vehicles in other countries will save their deposits. All these organisations are massively undercapitalised and in the end it will be the governments in all countries which step in.

We know of course, that the government has no money. They just print whatever they need. That leaves ordinary people taking the final burden of all this money printing.

But ordinary people will have no money either. Yes a few rich people will be taxed heavily to cover bank deficits and losses. Still, that will be a drop in the ocean. Instead ordinary people will be impoverished with little income, no government handouts, no pension and money which is worthless.

The above is sadly the cycle that all economic eras go through. The issue this time is that the problem is global and of a magnitude never seen before in history.

Regrettably a rotten and bankrupt financial system needs to go through a cleansing period which the world will now experience. There cannot be sound growth and sound values until the current corrupt and debt infested system implodes. Only then can the world grow soundly again.

The transition will sadly be dramatic with a lot of suffering for most people. But there is no other way. We won’t just see poverty, famine but also many human tragedies. The risk of social unrest or civil war is very high plus the risk of a global war.

Central banks had of course hoped that their Digital Currencies (CBDC) would be ready to save them (but not the world) from the present debacle by totally controlling people’s spending. But in my view they will be to late. And since CBDCs are just another form of Fiat money, it would just exacerbate the problem with an even more severe outcome at the end. Still, it won’t prevent them from trying.

MARKET VALUE OF US BANKING ASSETS $2 TRILLION LOWER THAN BOOK VALUE

A paper issued by 4 US academics in finance, illustrates the $2 trillion black hole in the US banking system:

“Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?”

March 13, 2023

Erica Jiang, Gregor Matvos, Tomasz Piskorski, and Amit Seru

CONCLUSION

“We provide a simple analysis of U.S. banks’ asset exposure to a recent rise in the interest rates with implications for financial stability. The U.S. banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets. We show that these losses, combined with a large share of uninsured deposits at some U.S. banks can impair their stability. Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to even insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. Overall, these calculations suggest that recent declines in bank asset values significantly increased the fragility of the US banking system to uninsured depositors runs.”

What is crucial to understand is that the $2 trillion “loss” is only due to higher interest rates. When the US economy comes under pressure, the loan books of the banks will deteriorate dramatically and bad debts increase exponentially. With total assets of US commercial banks at $23 trillion, I would be surprised if 50% is repaid or recoverable in the coming crisis.

The above risks are just for the US financial system. The global system will be no better with the EU under massive pressure partly due to US led sanctions of Russia. Virtually every major economy in the world is in a dire position.

Lets just look at the debt pyramid which I have discussed in many articles LINK

In 1971, when Nixon closed the gold window, global debt was $4 trillion. With gold backing no currency, this became a free for all to print unlimited amounts of money. And thus by 2000 debt had grown 25x to $100t. In 2006, when the Great Financial Crisis started, global debt was $120 trillion. By 2021 it had grown 75x from 1971 to $300 trillion.

The red column shows global debt at $3 quadrillion sometime between 2025 and 2030.

This assumes that the shadow banking system plus outstanding derivatives of currently probably around $2 quadrillion will need to be saved by central banks in a money printing bonanza. This will obviously lead to hyperinflation and thereafter to a depressionary implosion.

I know this sounds sensational but still a very likely scenario at the end of the biggest credit bubble in history.

GOLD – CRITICAL WEALTH PRESERVATION

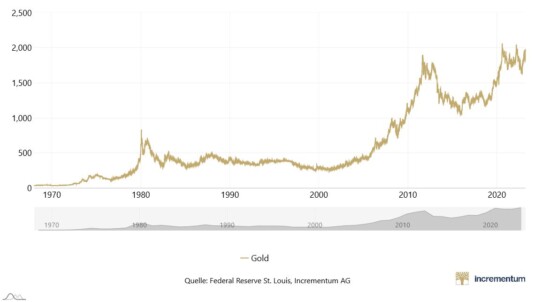

I have been standing on a soapbox for over 20 years, warning the world about the coming financial crisis and the importance of physical gold for wealth preservation purposes. In 2002 we invested important funds into physical gold with the purpose of holding it for the foreseeable future.

Between 2002 and 2011 gold went from $300 to $1,900. Since then gold corrected and then went sideways as stocks and the asset markets surged backed by massive credit expansion.

With gold currently around $1990, there is not much gain since 2011. Still since 2002 gold is up 7x. Due to the temporarily stronger dollar, gold’s gains measured in dollars are much smaller than in Euros, Pounds or Yen. But that will soon change.

In the final section of the article “WILL NUCLEAR WAR, DEBT COLLAPSE OR ENERGY DEPLETION FINISH THE WORLD?”, I outlined the importance of owning physical gold to store it in a safe jurisdiction away from kleptocratic governments.

“2023 is likely to be the year of gold. Both fundamentally and technically gold looks like it will make major up moves this year.”

And at the end of this article, I explain the importance of how and where gold should be held:“PREPARE FOR 10 YEARS OF GLOBAL DESTRUCTION.”

“So my own preference would be to own physical gold and silver that only I have direct control of and can withdraw or sell with very short notice.

It is also important to deal with a company that can move your metals at very short notice if the security or geopolitical situation would necessitate it.”

In February 2019 I wrote about what I called the Gold Maginot Line which had held for 6 years below $1,350. This is typical for gold. Having gone from $250 in 1999 to $1,900 in 2011, it then spent 8 years in a correction. At the time I forecast that the Maginot Line would soon break which it did and swiftly moved to $2,000 by August 2020. We have now had another period of consolidation since then and the next move above $2,000 and towards $3,000 is imminent.

Just to remind ourselves what happens to your money and gold during a hyperinflationary period, here is a photo from China’s hyperinflation in 1949 as people try to get their 40 grammes (just over one ounce) that they were allocated by the government. At some point in the next few years, there will be a panic in the West to buy gold at any price.

So as I have been urging investors for over 20 years, please get your gold NOW while it is still available.

STOP PRESS

Intense discussions are right now going on here in Switzerland between UBS, Credit Suisse, the regulator FINMA, the Swiss National Bank – SNB – and the Swiss Government. The Fed, the bank of England and the ECB are also involved.

The latest rumour is that UBS will buy Credit Suisse for CHF900 million ($1 billion). The shares of CS closed at a market cap of CHF8 billion on Friday. The deal would clearly involve backing from the SNB and the Swiss government which would have to take on major liabilities.

The December 2022 book value of CS was CHF42 billion, as with all banks massively overstated.

The deal isn’t done at this point, 5.30pm Swiss time, but the whole banking world knows that without a deal, there will be global contagion starting tomorrow Monday the 20th.

Even if a provisional deal will be done by Monday’s open, the financial system has now been permanently injured with an open wound which won’t heal.

The problem will just move on to the next bank, and the next and the next….

Hold on to your seats but buy gold first.