The following list of responses to frequently asked questions may assist you in understanding what is happening at SILICON VALLEY BANK.

On Friday, March 10, 2023, SILICON VALLEY BANK, SANTA CLARA, CA was closed by the CALIFORNIA DEPARTMENT OF FINANCIAL PROTECTION & INNOVATION. The Federal Deposit Insurance Corporation (FDIC) was then appointed Receiver. To protect the depositors, the FDIC created the Deposit Insurance National Bank of Santa Clara (DINB). The bank will be open for a LIMITED period of time providing LIMITED services.

HOW DO I FILE A CLAIM FOR UNINSURED FUNDS?

Depositors do not need to file a claim for deposit insurance. The FDIC uses the records of Silicon Valley Bank to make deposit insurance determinations. If you have less than $250,000 you do not need to file a claim.

WHAT IF MY ACCOUNT HAS GREATER THAN $250,000?

If you would like to check to see if your accounts are insured, please visit our Electronic Deposit Insurance Estimator (EDIE) https://edie.fdic.gov.

CAN I STILL USE BANKING SERVICES INCLUDING CHECKS, ATM, AND DEBIT CARDS?

Starting Monday, March 13, 2023, you may continue to use your personal checks; for a limited period of time.

You may use ATM/Debit cards for a limited period of time. You may continue to make deposits until the DINB closes. Online banking and bill pay services will not be available over the closing weekend, however, these services will resume Monday.

You may use ATM/Debit cards for a limited period of time. You may continue to make deposits until the DINB closes. Online banking and bill pay services will not be available over the closing weekend, however, these services will resume Monday.

PLEASE REMEMBER TO ACT QUICKLY TO REPLACE THESE SERVICES. We are currently determining end dates on the below items:

- AUTOMATIC PAYMENT and BILL PAY

- ATM/DEBIT CARD

- DIRECT DEPOSIT AND SOCIAL SECURITY

HOW DO I CLOSE MY ACCOUNT?

There are four ways to close your account:

- Create a bill pay or automated payment to another financial institution;

- Direct a wire transfer to another financial institution;

- Write a check for your available balance, then deposit that check into an account at another financial institution; or

- Ask for a “no fee” Cashier's check or Money Order by visiting your local branch during normal business hours.

NOTE: Please be sure to leave enough funds in your account to cover any outstanding checks.

If you prefer to speak with an FDIC Claims Agent call 1-866-799-0959 to schedule a telephone appointment.

CAN I USE ANY PORTION OF MY UNINSURED OR INSURED DEPOSITS TO REPAY A LOAN FROM SILICON VALLEY BANK?

In the event you have uninsured deposits, it may be possible to offset your uninsured amount against a loan in the same name as your uninsured deposit account. You should make a telephone appointment with an FDIC Claims Agent at 1-866-799-0959 to discuss your situation. If it is determined that you have some uninsured funds, the FDIC will mail you a Notice of Insurance Determination Letter (NIDL). The NIDL provides a Receiver’s Certificate Number which entitles you to share proportionately in any funds recovered through the sale of the assets of Silicon Valley Bank. You may eventually recover some of your uninsured funds as assets are liquidated. For an explanation of the dividend process and to review the status of receivership dividends call 1-866-799-0959.

WILL I GET AN ADVANCE DIVIDEND AND HOW DO I RECEIVE IT?

If you are an uninsured depositor, the FDIC will pay an advance dividend allowing you to access to a portion of their uninsured funds. The payment will be automatically added to your account, and you do not have to file a claim to receive it.

WHAT ABOUT MY AUTOMATIC PAYMENTS AND BILL PAY?

Any automatic payments from your account (unless there has been a hold placed on your account) will continue until you close your account or at the end of the DINB, whichever comes first. We encourage you to verify all automatic payments from your account the day after such payments are scheduled. You should move your automatic payments to a new bank as soon as possible.

Bill Pay will not be available over the closing weekend, however, it will be available for transactions on Monday, March 13, 2023. Any payments scheduled MUST CLEAR your account before the account is closed or at the end of the DINB, whichever occurs first. You should arrange a new online banking service promptly since this service will be discontinued.

WILL I RECEIVE INTEREST ON MY CERTIFICATES OF DEPOSITS (CDs)?

You will earn interest only through March 10, 2023. The FDIC has waived the early withdrawal penalty. If you had brokered CD accounts, you must contact your broker for further information.

WHAT ABOUT MY DIRECT DEPOSITS?

All direct deposits, including Social Security deposits, will continue until the end of the DINB, however, you should arrange to move any automatic deposits or withdrawals as soon as possible. The institution of your choice will be glad to assist you in completing the required documentation.

Direct deposits from anyone other than the Federal government cannot be redirected. You must contact the sender and arrange for these deposits to be made to another financial institution.

If you have federal benefits, including Social Security, you may also find assistance by visiting www.godirect.gov. The Social Security Administration can be contacted at www.ssa.gov/deposit/.

WHAT HAPPENS IF A HOLD IS PLACED ON MY ACCOUNT?

An account hold may be placed on an account(s) if there is a need for additional documentation from a depositor. For example, a Declaration for Trust form may be required to attest to the parties involved in a trust.

It is possible a depositor's account was held due to delinquent loans where the depositor is the borrower or guarantor. Additionally, any account pledged as collateral for a loan will continue to be held. A letter will be sent informing you of any holds placed by the FDIC, along with instructions on how to proceed. If you have any questions regarding these holds, please call the FDIC at the number provided in the letter or contact the FDIC at 1-866-799-0959 to schedule a telephone appointment.

WHAT HAPPENS TO MY IRA ACCOUNT?

IRA deposits are insured separately from all other accounts up to $250,000. You have 60 days to reinvest this deposit/distribution into another retirement vehicle to qualify as a rollover for income tax purposes. You should consult IRS Publication 590 and/or your tax advisor concerning the possible tax consequences of this distribution. IRS Publication 590 addresses this type of bank failure and may be obtained at www.irs.gov or by contacting your local IRS office.

DO I HAVE TO MAKE MY LOAN PAYMENTS?

You should continue to make your loan payments to the same address as you have in the past. Make your check payable to Silicon Valley Bank. All escrow services previously performed related to your loan will continue. Should you receive notification that any portion of your taxes or insurance was not paid, please notify your loan officer immediately. You should direct your loan questions to your loan officer.

It is the FDIC's intention to sell all loans, and it will be up to the new owner to determine the best method to collect the loan. If your loan is sold, you will be notified by mail in advance of the sale. You have the right to refinance your loan with another institution.

At this point, the FDIC will suspend foreclosure actions to evaluate the loans and the borrower’s ability to repay. There may be instances where the FDIC will continue with the foreclosure process, but this will be done on a case-by-case basis.

If you need to contact an FDIC Loan Representative you may:

- Call the FDIC Customer Service number at 1-866-799-0959.

- Send an email to FDIC_Loans@fdic.gov.

- Contact Us at FDIC.gov or the support center link: https://ask.fdic.gov/fdicinformationandsupportcenter/s/.

ARE MY SILICON VALLEY BANK CHECKS STILL VALID?

Merchants and others are encouraged to honor Silicon Valley Bank checks, as these checks will continue to clear up to the insured available balance until the end of the DINB. A copy of this document or the press release from www.fdic.gov can be provided since both documents indicate that insured deposits have been received by the DINB. Additional copies will be available at your local bank branch. Depositors or merchants can also call the FDIC at 1-866-799-0959 or contact staff at your former Silicon Valley Bank branch locations to confirm this information.

WILL MY OFFICIAL CHECK ISSUED BY SILICON VALLEY BANK CLEAR?

Interest checks and cashier's checks will continue to clear up to the insurance limit until the DINB end date. Cashier's checks and interest checks outstanding as of March 10, 2023, are eligible for deposit insurance coverage and will be added back to any of your other account balances with the same ownership capacities to determine your insurance coverage. If a portion of an interest check or cashier’s check exceeds the insurance limits, a stop payment order may have been issued on that check. If you believe that a check in your possession exceeds the deposit insurance limits, you may call the FDIC Call Center at 1-866-799-0959 to schedule a telephone appointment to speak to an FDIC Claims Agent.

CAN I OVERDRAFT MY ACCOUNT OR USE A LINE OF CREDIT?

The DINB will not allow overdrafts. Any checks overdrawing an account prior to Monday, March 13, 2023, will be returned unpaid. ALL LINES OF CREDIT, including home equity lines, will be permanently frozen as of the closing on March 10, 2023. You will need to establish a new line of credit with your new bank.

CAN I STILL USE MY SAFE DEPOSIT BOXES?

You must close and empty your safe deposit box by the end of the DINB. After that date, you will be required to make an appointment by calling 1-866-799-0959. For safety reasons, you are encouraged to secure a new safe deposit box prior to emptying your box. If you do not clear your safe deposit boxes by the end of the DINB, the box will be drilled under dual control. The contents will be escheated according to state law. A letter will be sent to you at the address listed on the bank’s record prior to your box being drilled. After the end of the DINB, the current disposition of your safety deposit box can be obtained by calling 1-866-799-0959. Unclaimed property can be located by visiting www.missingmoney.com or by contacting the State Treasurer’s office or the office of unclaimed property.

If you prepaid your safe deposit box rental fees, you may file a claim with the Receiver to recover the unused fees. A letter explaining the claims process and the Proof of Claim form will be mailed to you.

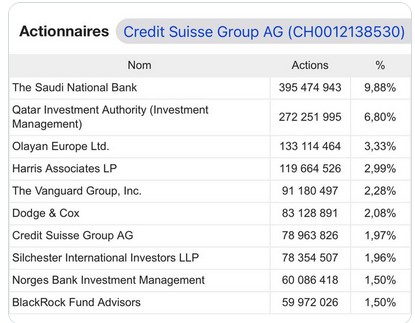

I AM A SHAREHOLDER, WHAT DO I DO?

The holding company, SVB Financial Group, Santa Clara, CA, owns all shares of bank stock. The holding company was not included in the closing of the bank or the resulting receivership. If you are a shareholder of the holding company, please do not contact or file a claim with the Receiver. You must contact the holding company directly for more information.

SVB Financial Group

3003 Tasman Dr.

Santa Clara, CA 95054

3003 Tasman Dr.

Santa Clara, CA 95054

WILL I RECEIVE MY BANK STATEMENTS AND OTHER ACCOUNT INFORMATION?

The DINB will mail your account statements at the same time you have received them in the past. Customers who have not closed their accounts by close of business the day of the end of the DINB will receive a final statement approximately one week after the DINB closing date. Please call or visit your branch to request any records you may need. After the DINB end date, please call 1-866-799-0959 for assistance.

HOW WILL I GET MY 1098/1099s FOR TAX REPORTING?

The FDIC as Receiver for Silicon Valley Bank will be responsible for mailing your 1099 tax information. Your 1098 reporting will be done by the FDIC as Receiver for Silicon Valley Bank or the servicer of your loan.

WHAT IF SILICON VALLEY BANK OWES ME MONEY, HOW DO I FILE A CLAIM?

Creditors must submit claims in writing, together with proof of the claim, on or before the claims bar date, to be determined. However, potential claimants should call 1-866-799-0959 to discuss the process for filing a claim with a Claims Agent. To file a claim please send it to the following address:

FDIC as Receiver for Silicon Valley Bank

600 N. Pearl St., Suite 700

Dallas, Texas 75201

600 N. Pearl St., Suite 700

Dallas, Texas 75201

SHOULD I BE WORRIED ABOUT SCAMS?

Please be advised you will not receive any communications from the FDIC requesting any private information. Be watchful for and resistant to any scams to obtain information from you by individuals or entities stating they are acting on behalf of Silicon Valley Bank or the FDIC. Should you be contacted by anyone requesting private information from you related to this event, please contact the FDIC Call Center at 1-866-799-0959.

ADDITIONAL QUESTIONS: Please contact the FDIC Call Center at the number provided below with any additional questions:

1-866-799-0959

FDIC CALL CENTER HOURS OF OPERATION – ALL HOURS ARE Pacific Time

Friday, March 10, 2023: Until 9:00 PM

Saturday, March 11, 2023: 9:00 AM – 6:00 PM

Sunday, March 12, 2023: 12:00 PM – 6:00 PM

Monday, March 13, 2023: 8:00 AM – 8:00 PM

Thereafter: 9:00 AM – 5:00 PM

Saturday, March 11, 2023: 9:00 AM – 6:00 PM

Sunday, March 12, 2023: 12:00 PM – 6:00 PM

Monday, March 13, 2023: 8:00 AM – 8:00 PM

Thereafter: 9:00 AM – 5:00 PM

Additional information: https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/index.html.